Featured

Table of Contents

A technique you follow beats a technique you abandon. Missed out on payments produce costs and credit damage. Set automated payments for every card's minimum due. Automation secures your credit while you focus on your chosen reward target. Then manually send out extra payments to your priority balance. This system lowers stress and human error.

Look for realistic changes: Cancel unused memberships Lower impulse costs Prepare more meals in your home Sell products you don't utilize You do not need extreme sacrifice. The objective is sustainable redirection. Even modest extra payments substance gradually. Expense cuts have limitations. Earnings development expands possibilities. Consider: Freelance gigs Overtime shifts Skill-based side work Selling digital or physical goods Treat additional earnings as debt fuel.

Believe of this as a temporary sprint, not a long-term lifestyle. Financial obligation reward is psychological as much as mathematical. Many plans fail since inspiration fades. Smart mental techniques keep you engaged. Update balances monthly. Seeing numbers drop enhances effort. Paid off a card? Acknowledge it. Small benefits sustain momentum. Automation and regimens reduce decision tiredness.

Reviewing Proven Debt Programs for 2026

Behavioral consistency drives effective credit card financial obligation reward more than perfect budgeting. Call your credit card provider and ask about: Rate decreases Difficulty programs Promotional deals Lots of loan providers prefer working with proactive clients. Lower interest implies more of each payment hits the principal balance.

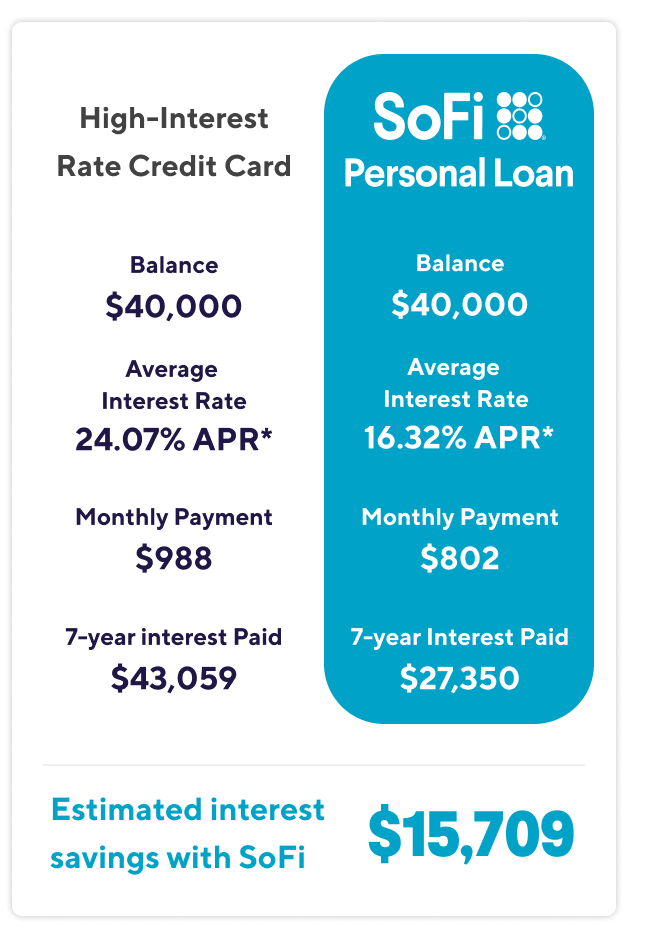

Ask yourself: Did balances diminish? Did spending stay managed? Can extra funds be redirected? Adjust when required. A flexible plan survives reality better than a rigid one. Some circumstances need additional tools. These choices can support or change standard reward techniques. Move debt to a low or 0% introduction interest card.

Combine balances into one set payment. Works out reduced balances. A legal reset for frustrating debt.

A strong financial obligation technique U.S.A. homes can rely on blends structure, psychology, and flexibility. Financial obligation reward is rarely about severe sacrifice.

Smartest Strategies to Clear Debt for 2026

Paying off credit card financial obligation in 2026 does not need excellence. It needs a wise plan and consistent action. Snowball or avalanche both work when you devote. Mental momentum matters as much as math. Start with clarity. Construct security. Pick your technique. Track progress. Stay patient. Each payment reduces pressure.

The smartest move is not awaiting the perfect minute. It's beginning now and continuing tomorrow.

In discussing another prospective term in office, last month, previous President Donald Trump stated, "we're going to pay off our debt." President Trump likewise assured to pay off the nationwide financial obligation within 8 years throughout his 2016 governmental campaign.1 It is difficult to know the future, this claim is.

Over four years, even would not suffice to pay off the debt, nor would doubling revenue collection. Over 10 years, settling the financial obligation would need cutting all federal costs by about or enhancing income by two-thirds. Presuming Social Security, Medicare, and defense costs are exempt from cuts constant with President Trump's rhetoric even getting rid of all staying spending would not pay off the financial obligation without trillions of extra earnings.

Smartest Methods to Eliminate Debt for 2026

Through the election, we will release policy explainers, reality checks, budget scores, and other analyses. At the beginning of the next governmental term, debt held by the public is most likely to amount to around $28.5 trillion.

To achieve this, policymakers would require to turn $1.7 trillion typical annual deficits into $7.1 trillion yearly surpluses. Over the ten-year spending plan window starting in the next presidential term, covering from FY 2026 through FY 2035, policymakers would need to accomplish $51 trillion of spending plan and interest cost savings enough to cover the $28.5 trillion of preliminary financial obligation and avoid $22.5 trillion in financial obligation accumulation.

It would be literally to pay off the financial obligation by the end of the next presidential term without big accompanying tax boosts, and likely difficult with them. While the needed savings would equal $35.5 trillion, overall spending is projected to be $29 trillion over that four-year period of which $4 trillion is interest and can not be cut directly.

Improving Financial Literacy Through Proven Programs

(Even under a that presumes much quicker economic development and considerable new tariff profits, cuts would be nearly as big). It is also likely impossible to attain these savings on the tax side. With overall income expected to come in at $22 trillion over the next governmental term, income collection would need to be almost 250 percent of present projections to settle the national debt.

Although it would need less in annual cost savings to settle the nationwide debt over 10 years relative to four years, it would still be almost difficult as a useful matter. We estimate that paying off the debt over the ten-year spending plan window between FY 2026 and FY 2035 would need cutting costs by about which would lead to $44 trillion of main spending cuts and an extra $7 trillion of resulting interest savings.

The job becomes even harder when one considers the parts of the spending plan President Trump has actually removed the table, along with his call to extend the Tax Cuts and Jobs Act (TCJA). President Trump has committed not to touch Social Security, which indicates all other spending would have to be cut by nearly 85 percent to fully eliminate the national debt by the end of FY 2035.

If Medicare and defense costs were likewise excused as President Trump has sometimes for spending would have to be cut by nearly 165 percent, which would certainly be impossible. To put it simply, investing cuts alone would not be enough to settle the national financial obligation. Huge boosts in earnings which President Trump has actually normally opposed would also be needed.

Analysing Top-Rated Credit Options for 2026

A rosy circumstance that incorporates both of these doesn't make paying off the debt much simpler.

Importantly, it is extremely unlikely that this income would emerge. As we've written before, achieving continual 3 percent economic growth would be exceptionally challenging on its own. Since tariffs typically slow economic growth, achieving these 2 in tandem would be even less most likely. While no one can understand the future with certainty, the cuts required to pay off the financial obligation over even 10 years (let alone 4 years) are not even near practical.

{kind=link}

Latest Posts

How Nonprofit Programs Simplify Payments in 2026

How to Merge Multiple Debt in 2026

Comparing Counseling versus Loans in 2026